The vaping industry has grown substantially over the past two decades, becoming a well-established segment of the nicotine market. Vaping products offer adult consumers a significantly less harmful alternative to combustible cigarettes—especially for those seeking to quit smoking or reduce their exposure to harmful substances.

A wide array of vapor products and electronic nicotine delivery systems (ENDS) are available on the market. Open-system devices allow users to refill them with various e-liquids, offering customization and greater control over flavor and strength. Closed-system products, on the other hand, utilize pre-filled, non-refillable cartridges or pods. These devices are simpler to use and have grown increasingly popular, but many of them remain unauthorized for sale in the United States by the Food and Drug Administration (FDA).

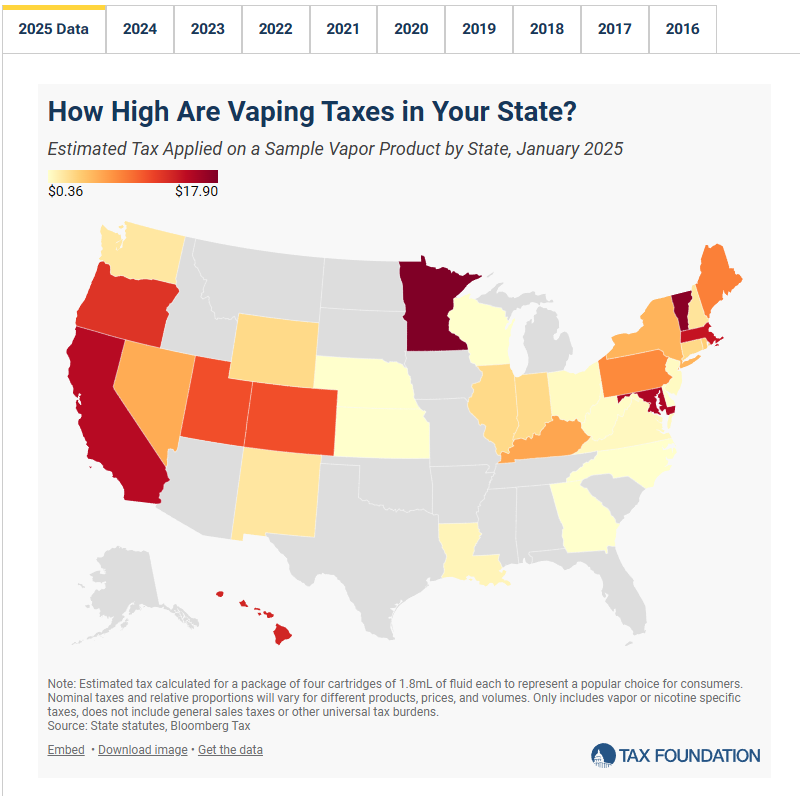

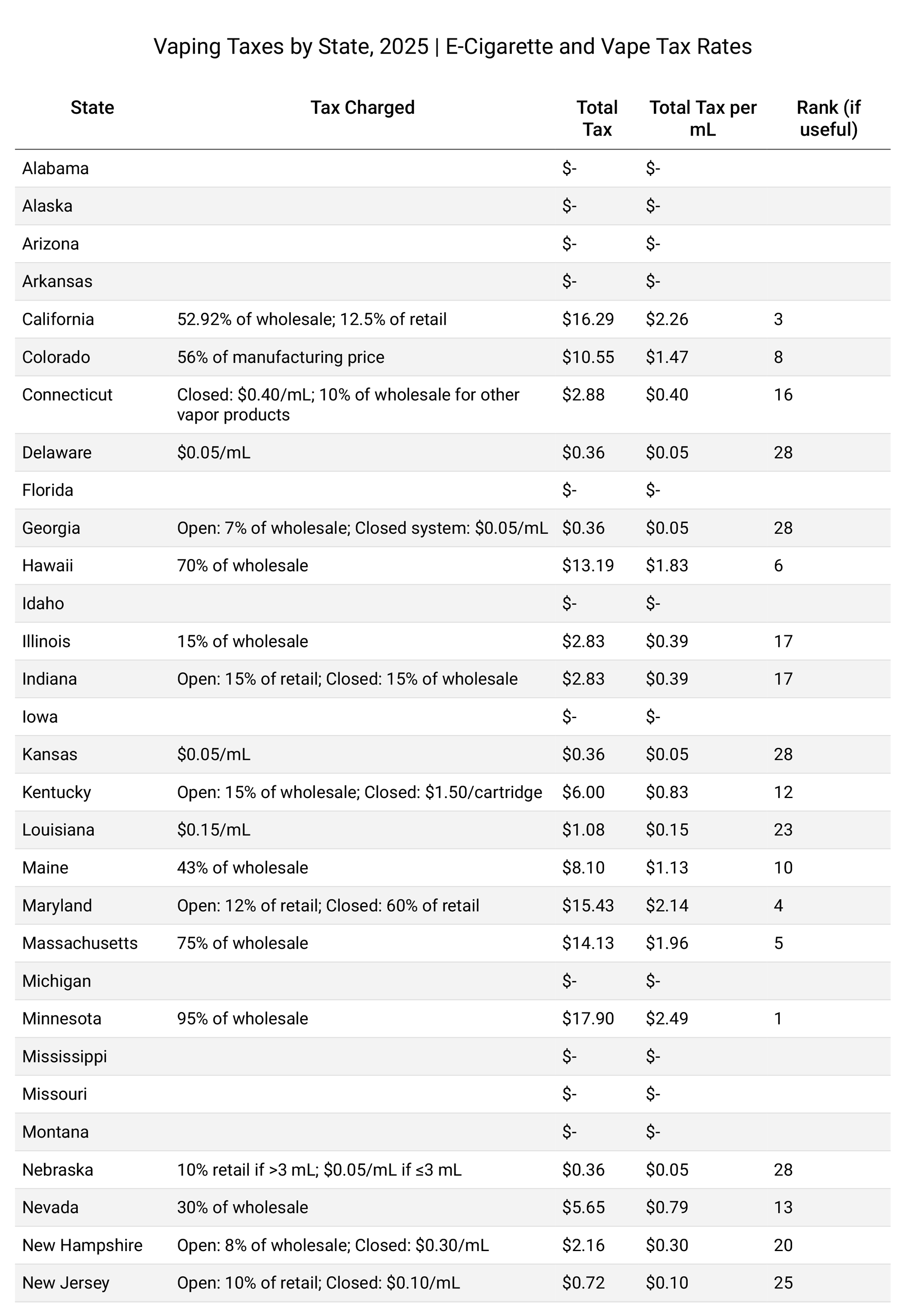

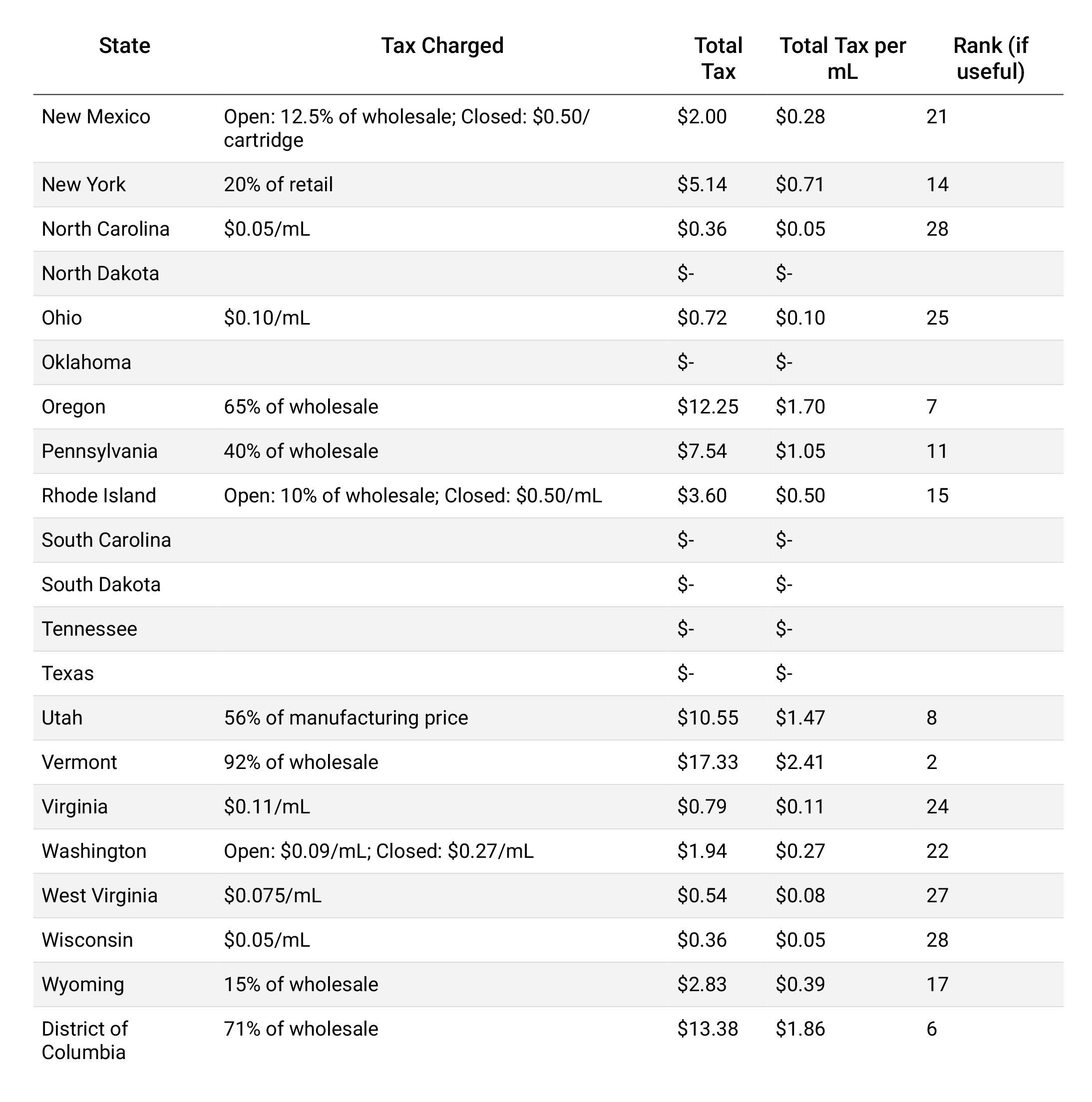

As of January 2025, 33 states and the District of Columbia levy excise taxes on vapor products. Tax structures vary widely across states and can be applied based on manufacturer price, wholesale or retail price (ad valorem), or product volume (specific tax). Some states also use bifurcated systems, taxing open and closed systems differently.

This variation makes it difficult to compare tax burdens across jurisdictions. To address this, the Tax Foundation calculated each state's tax on a sample product: a 4-pack of 1.8 mL closed-system cartridges, with a wholesale price of $18.84, assuming a 5% wholesale markup and a 30% retail markup.

California reduced its wholesale tax rate from 56.32% to 52.92%.

Colorado increased its manufacturing tax from 50% to 56%.

The District of Columbia reduced its wholesale tax from 79% to 71%.

Rhode Island enacted a new tax: 10% of wholesale for open systems and $0.50/mL for closed systems.

Virginia increased its per-milliliter tax from $0.066 to $0.11/mL.

Minnesota imposes the highest overall tax burden—$17.90 per 4-pack, equivalent to $2.49/mL, with a 95% wholesale rate.

Vermont and California follow, with $17.33 and $16.29, respectively.

Delaware, Georgia, Kansas, Nebraska, North Carolina, and Wisconsin have the lowest tax at $0.36, based on a flat $0.05/mL rate.

Maryland applies the highest retail tax rate at 60% on closed systems.

Rhode Island has the highest volume-based rate at $0.50/mL, followed by Connecticut ($0.40/mL) and New Hampshire ($0.30/mL).

Some states, including Florida, Texas, Michigan, and others, do not currently tax vapor products.

Tax policy plays a pivotal role in influencing consumer behavior. High taxes on vaping products, which are demonstrably less harmful than combustible cigarettes, can deter smokers from switching and inadvertently undermine public health efforts. For instance, Minnesota’s 95% wholesale tax has been linked to over 32,000 fewer smokers quitting, compared to states with lower rates.

Leading health authorities, including Public Health England and King’s College London, have concluded that vaping is approximately 95% less harmful than smoking. These findings underscore the importance of harm reduction—the concept that policies should aim to reduce harm rather than eliminate risk, especially when total abstinence is unrealistic.

Sound excise tax design should reflect the relative risk of each nicotine product. Over-taxing vapor products, especially while maintaining lower taxes on traditional cigarettes, is counterproductive. Such policies may not only discourage switching but also drive consumers to illicit markets, where products are unregulated, untaxed, and potentially unsafe.

An optimal regulatory and tax framework would:

Support harm reduction goals

Encourage smokers to transition to safer alternatives

Limit black market growth

Generate sustainable tax revenues

Protect adult consumer choice

Vapor products represent an opportunity to significantly reduce smoking-related deaths. Policies that enable, rather than obstruct, harm reduction could yield substantial public health and economic benefits.

vapeMons.co is the official wholesale and retail vape platform, offering a trusted and comprehensive solution for businesses and individual customers alike. From wholesale vape juice and nicotine salts to starter kits, disposables, and accessories, we serve global distributors, vape shops, e-commerce vendors, and retail consumers. At vapeMons, we are committed to supporting adult smokers in finding less harmful alternatives—combining innovation, quality, and style in everything we do.

FDA Disclaimer

The statements regarding these products have not been evaluated by the Food and Drug Administration. These products are not intended to diagnose, treat, cure, or prevent any disease or medical condition. The efficacy of these products and the testimonials provided have not been confirmed by FDA-approved research. All information presented is for general informational purposes only and is not intended as a substitute for professional medical advice, diagnosis, or treatment. Please consult your healthcare provider before using any product, especially if you are pregnant, nursing, taking medication, or have any medical condition. The Federal Food, Drug, and Cosmetic Act requires this notice. vapeMons makes no health claims regarding its products and assumes no responsibility for any medical claims made in customer testimonials. Improper use of these products is not the responsibility of vapeMons. We strongly recommend consulting a qualified medical professional before beginning any health-related regimen. You must be 21 years of age or older to access this website and/or purchase vapeMons products.

THC Disclaimer

Products on this site contain no more than 0.3% Δ9-THC on a dry weight basis, in compliance with federal law. These statements have not been evaluated by the Food and Drug Administration. This product is not intended to diagnose, treat, cure, or prevent any disease. Do not use if you are pregnant, nursing, have a medical condition, or are taking any medications. Always consult your healthcare provider before use. Keep out of reach of children and pets. This product may impair your ability to drive or operate machinery.

Nicotine Disclaimer

Nicotine products are intended for use by adults age 21 and over. Sale to minors is strictly prohibited. Not intended for use by individuals under the legal age, or by pregnant or breastfeeding women. Keep out of reach of children and pets. Nicotine is not intended to diagnose, cure, mitigate, treat, or prevent any disease. It is intended solely as a satisfying alternative for adult vapor consumers. This is a finished product and should not be mixed with nicotine-containing e-liquids.